Bottom Line Up Front: I’m staying put at 50% C-Fund / 50% S-Fund.

The last couple weeks gave us a real scare — a sharp pullback followed by an equally sharp rebound — but the reasons I’m in this mix haven’t changed: AI-driven growth is still lifting both large caps and small caps, even with chip stocks getting knocked around, and I want exposure to that upside. The Middle East situation is the thing keeping me from going further out on a limb, though — that kind of instability has a way of spilling into international markets, and I’d rather stay domestic-heavy while that plays out.

Let me walk you through what actually happened, because the headline “market was flat for the month” hides a genuinely wild couple of weeks underneath. NOTE: Historically speaking, “summer” is always weak, performance-wise, for the US markets. August, is the worst, in almost all years since 1987. So welcome to August, and just hang in there little fellers.

The Recap

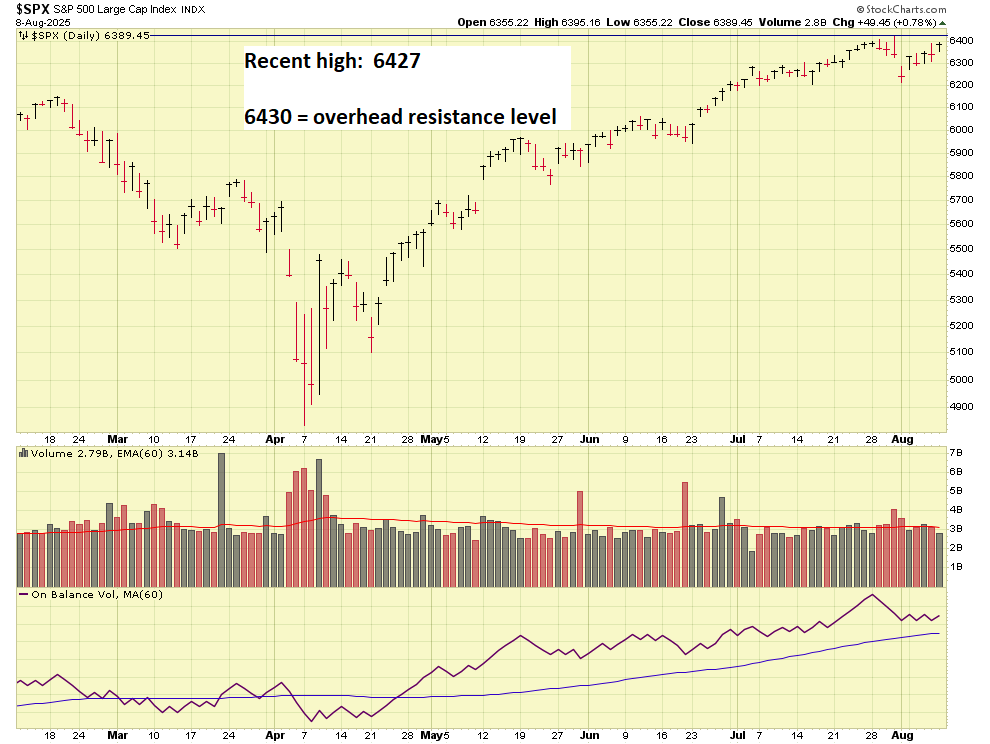

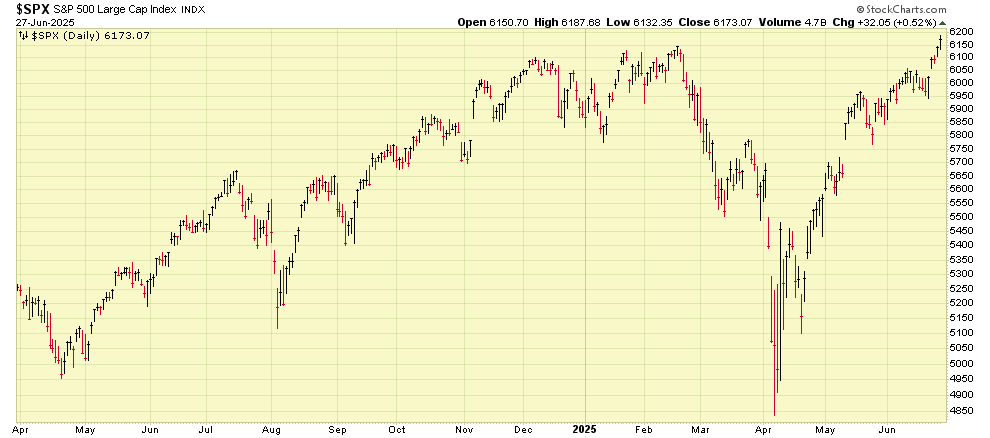

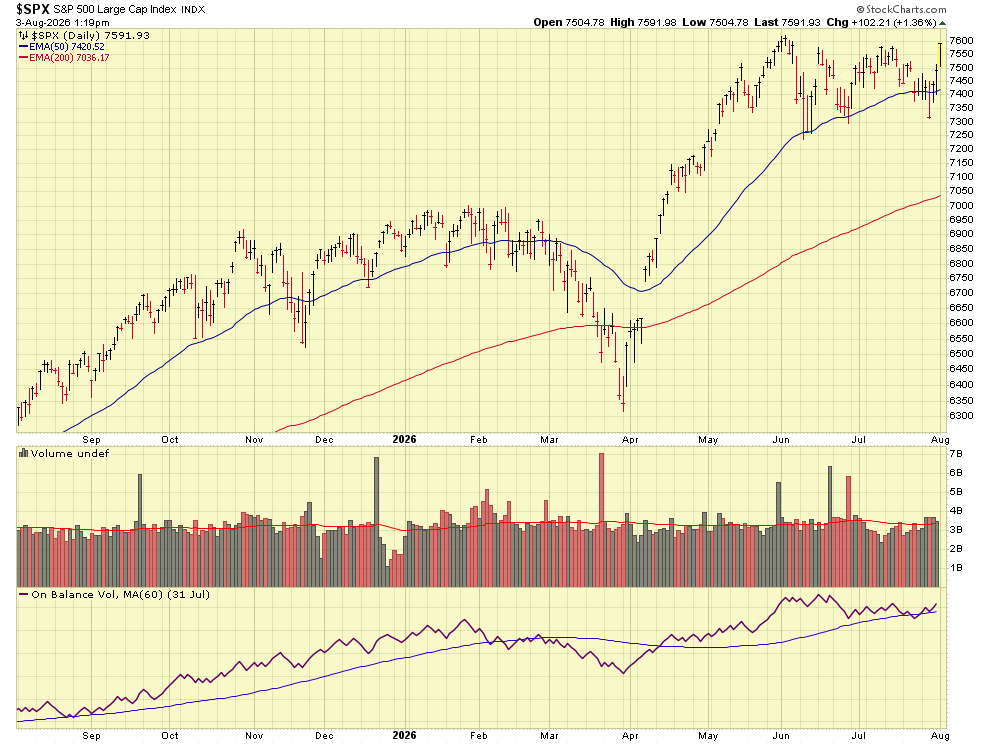

Things came to a head on July 29, the day the Fed announced its rate decision. The S&P 500 dropped to 7,316, the Dow fell to 51,594 (over 1,100 points, its worst day since April), and the Nasdaq slid to 24,443. That’s a rough day by any measure. But markets don’t like uncertainty more than they dislike bad news, and once the Fed decision was out and digested, buyers came back in a hurry. By July 31 — the last trading day of the month — the S&P had climbed all the way back to 7,489.72, the Dow to 52,485.03, and the Nasdaq to 25,373.85. Net for the month, the S&P ended up basically flat, and the Dow actually notched its fourth straight positive month, which tells you the “boring” blue-chip names held up better than the flashier tech trade this time around. See chart of S&P 500:

Two stocks tell the story of that final Friday rally almost by themselves. Or, in plain English, two stocks basically were entirely responsible for the “comeback.” Which means an “up day” or “rally” should always trigger a deeper analysis as to why it rallied. Broad, positive economic news? Or isolated, one-off reasons? Should we “jump back in” based on the rally? Etc should all be asked.

Amazon jumped hard on a strong cloud-computing earnings report — the kind of number that reminds investors the AI infrastructure buildout is, at least for some companies, actually turning into revenue. Apple, on the other hand, fell on a weaker forward outlook — proof that even inside the same “Magnificent Seven” club, results can pull in completely opposite directions depending on what a company tells investors about what’s coming, not just what already happened. Personal soap box but Apple is way behind on everything AI. Asking Siri to perform a task is like asking talking to a 2008 model Furby doll. Apple needs to get their act together on AI. Ok, I digress….

Ongoing market challenges

A handful of things are worth understanding here, and I’ll try to keep the jargon to a minimum.

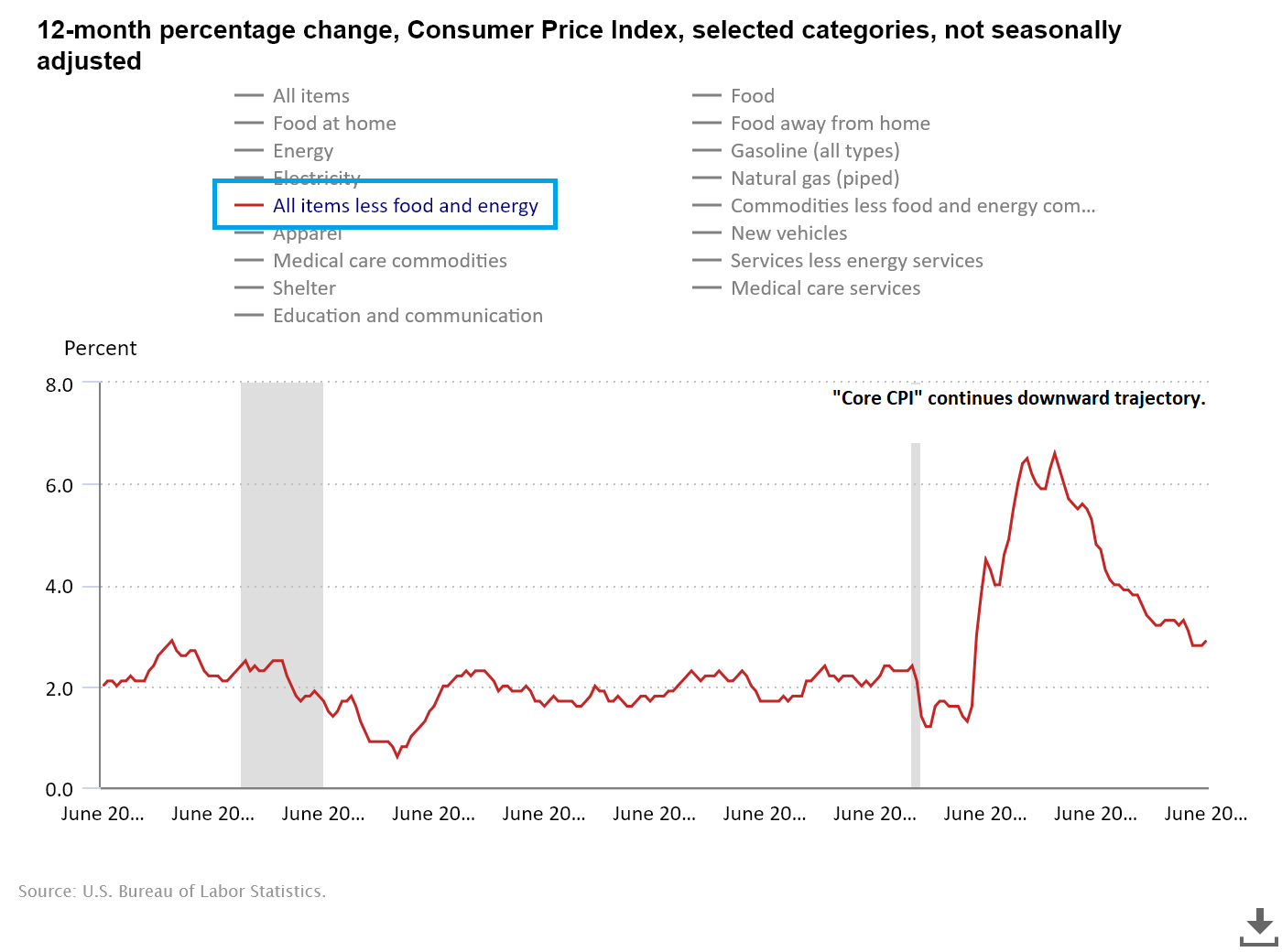

First, inflation. The Fed’s preferred inflation gauge (PCE) actually cooled in June — headline came in at 3.7% year-over-year, down from May’s 4.1%, and the core reading (which strips out food and energy) eased to 3.3% from 3.4%. That’s genuinely good news on its face. The catch: a lot of that cooling was tied to a temporary truce in the Iran conflict that pulled energy prices down for a stretch — and that truce has since broken down, with fighting resuming in July. So don’t get too comfortable with the “inflation is cooling” story until we see how July’s number holds up.

Second, the Fed itself. They held rates steady at 3.50%–3.75% for the fourth time this year, but the vote wasn’t unanimous — three members wanted to raise rates instead of holding. That’s a meaningful split for a committee that’s supposed to be reading the same data. Compounding that, new Fed Chair Kevin Warsh has been noticeably terser in his communications than his predecessor — shorter statements, less forward guidance about where rates are headed next.

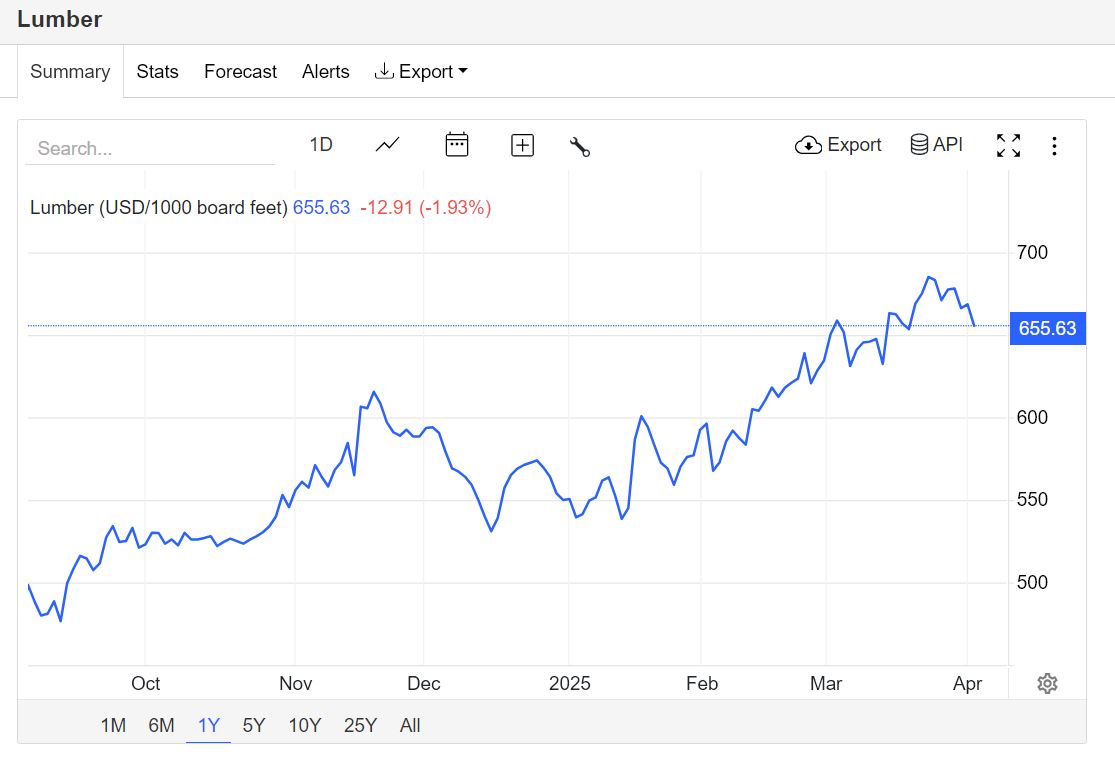

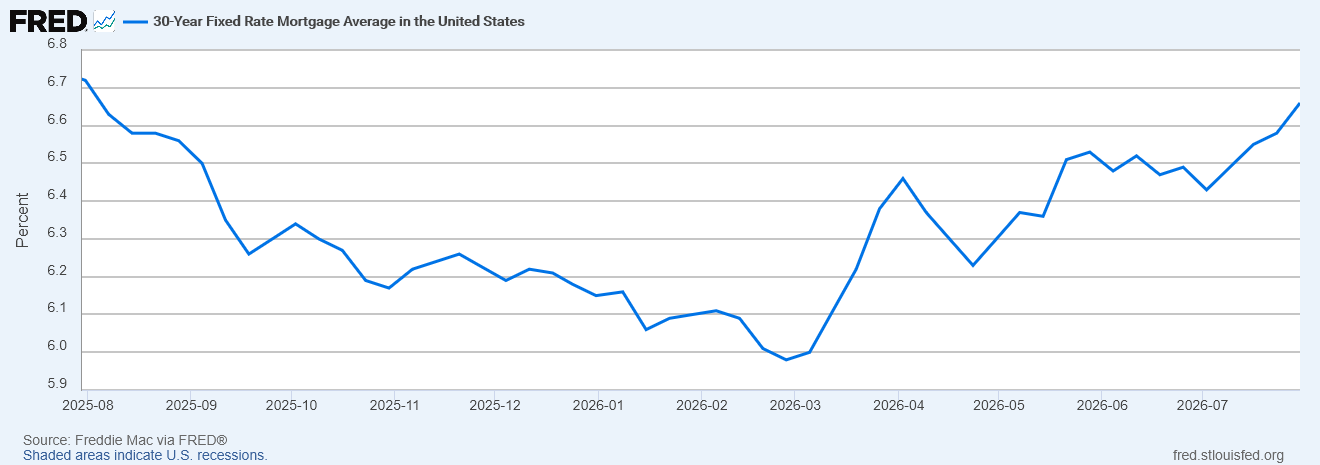

Here’s an interesting wrinkle worth sitting with: Warsh was President Trump’s own pick for the job, nominated after a public and pointed campaign by the administration for lower rates. But the data he’s inherited hasn’t cooperated with that wish — inflation is still running well above target, oil prices are elevated again, and three of his own committee members just voted for a hike, not a cut. In my opinion, that makes it genuinely hard to see rates coming down anytime soon, regardless of who’s in the chair. If anything, the near-term pressure looks tilted toward holding steady or even raising, not cutting. The next scheduled Fed meeting is September 15–16, and I’ll be watching closely to see whether the data between now and then changes that picture. Amongst other things, this affects mortage rates, which are near all-time highs, primarily because of inflation risks tied to energy/geopolitics and a cautious Fed, which keep Treasury yields (and the mortgage spread on top of them) elevated. Rates can move quickly with changes in oil prices, inflation data, Fed signals, or geopolitical developments. See chart:

Third, longer-term interest rates have been climbing on their own, separate from anything the Fed is doing directly. The 10-year Treasury yield has been running in the 4.65%–4.75% range, and the 30-year hit its highest level since 2007. Even if the Fed keeps the “official” rate steady, if long-term borrowing costs keep drifting higher anyway, that still acts like a headwind on stock valuations — especially for growth-heavy tech names that depend on cheap money to justify big future earnings promises. That’s a meaningful part of why chip and semiconductor stocks in particular have had a rough stretch, with the Nasdaq 100 dipping into correction territory (a drop of more than 10% from its recent peak). I don’t think this unwinds the broader AI growth story — but it’s the piece of this market I’m watching most closely right now.

Fourth, elevated oil prices. Renewed tension in the Middle East pushed crude higher again in late July, and that matters for two reasons: it’s inflationary on its own, and it adds to the argument that the Fed can’t afford to get too comfortable declaring victory just yet. This is the same reasoning behind why I’m staying domestic in my own allocation — when oil and geopolitics get twitchy like this, it tends to hit international and emerging markets harder and faster than it hits U.S. large- and small-caps, so I’d rather not add that extra layer of risk to my own TSP mix right now.

Last, worth a mention: a decent chunk of July’s index-level strength was carried by a handful of mega-cap names rather than the broad market. When gains concentrate that heavily in a few stocks, it’s worth remembering that the calm at the index level can mask more turbulence underneath — something worth keeping in mind if you’re diversified across the C and S Funds like I am.

The Economy, Broadly

Growth is still positive, just not as fast as earlier in the year. Second-quarter GDP came in at 1.5% annualized, down from 2.1% in the first quarter. That’s a deceleration, not a collapse — consumer spending and business investment (a fair amount of it AI-related) both still grew, it’s just that the pace slowed. I wouldn’t read too much doom into one quarter’s slowdown, but it’s one more data point suggesting we’re past the “sprint” phase of this expansion and into something more like a jog.

What I’m Watching Next

Two big releases are still ahead of us as I write this. The next jobs report, and the next (CPI and PCE) inflation reading. Either one — a weak jobs number, or an inflation print that shows oil’s recent climb bleeding into the broader numbers — could easily reshape the conversation heading into that September Fed meeting. I don’t have a strong prediction to offer you here, and honestly, if I’m being straight with you, I’ve been wrong before trying to call these short-term data surprises. My better track record has been in sticking to a sensible allocation and letting these swings play out rather than trying to trade around them.

That’s really the core of my philosophy here, and it’s worth repeating: I’m not trying to time this market. I’m rebalancing occasionally based on where I think the multi-month picture is headed, and right now that picture still says: stay invested in U.S. equities to capture the AI-driven growth story, but keep some caution baked in around anything with heavy international exposure given how unsettled things still are overseas. All of this of course, is my opinion. The I-Fund could return 500% next month for all I know. Again (did I say this?) this is my opinion.

Thanks for reading. Talk to you soon.

-Bill Pritchard

This is for informational purposes only and is not investment advice. Please consult a financial advisor or other licensed professional before making changes to your own TSP allocation.