Hello Folks

In true “no news is good news fashion”, I simply had no bad news to write about, or “warning signs” observed this month so far – this is my second October post, albeit at the end of the month. As such, it will serve as my opinion based analysis on what happened, and what lies ahead. Bottom Line Up Front: My TSP Allocation and Contributions of 50% C-Fund, 50 % I-Fund remains unchanged, I will discuss that in a little while.

First, as reported by some of the Government Employee targeted websites out there (Federal News Radio, Government Executive, NARFE, etc): The 2018 joint budget resolution was passed with no cuts to federal retirement, pay, or other benefits.

With that said, for deeper, more knowledgeable insight into the benefits related perspective and the respective proposed cuts, subscribe to retired FBI S/A and current CPA Dan Jamison’s FERS GUIDE. A paid subscriber will get email access to Dan who will attempt to answer your questions. Every couple of weeks Dan and I trade emails in regards to benefits and/or TSP, he is the expert in regards to retirement benefits knowledge.

As it stands, no cuts have occurred however we may see this topic rear its head again down the road. My opinion is this “flare up” should serve as a gear/equipment check for the folks in the audience, take a look at your financial situation: if you are eligible to retire now (or soon), then apply that risk-assessment we all do in our day jobs. I don’t think anyone has the answer, but I think that “Already-Retired status” is more insulated from attempts to erode your benefits than not.

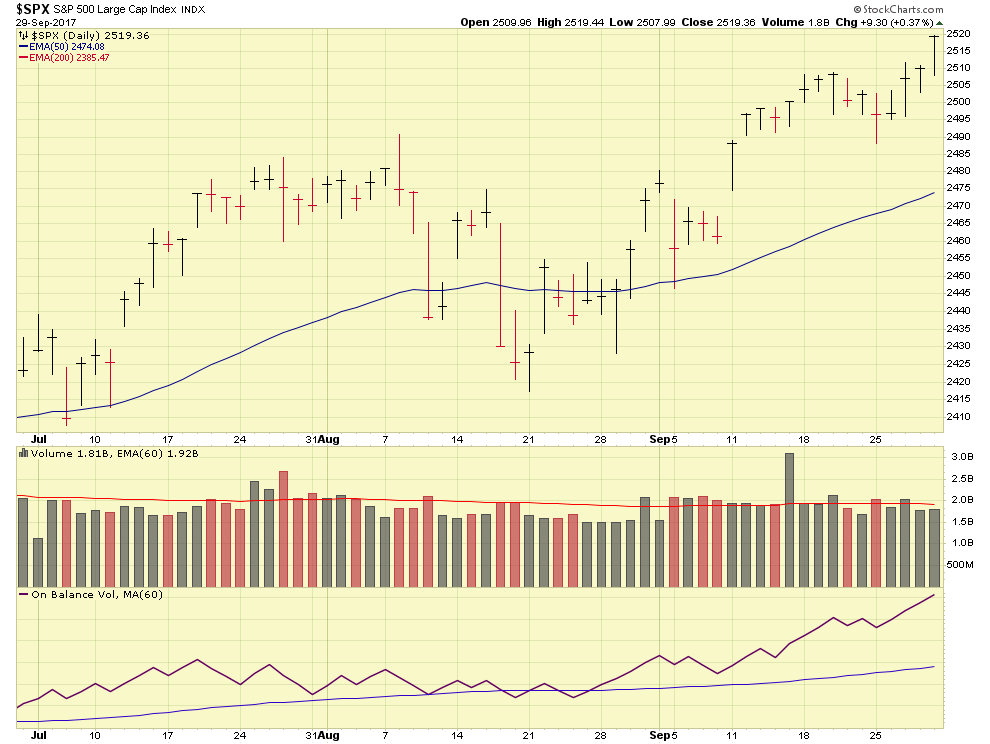

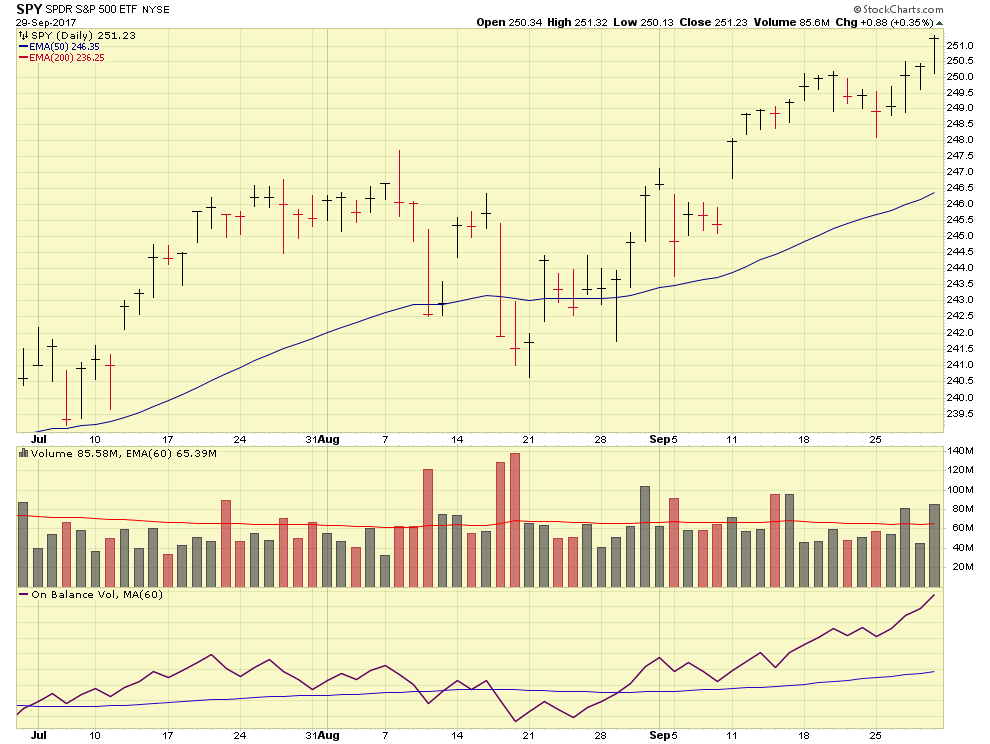

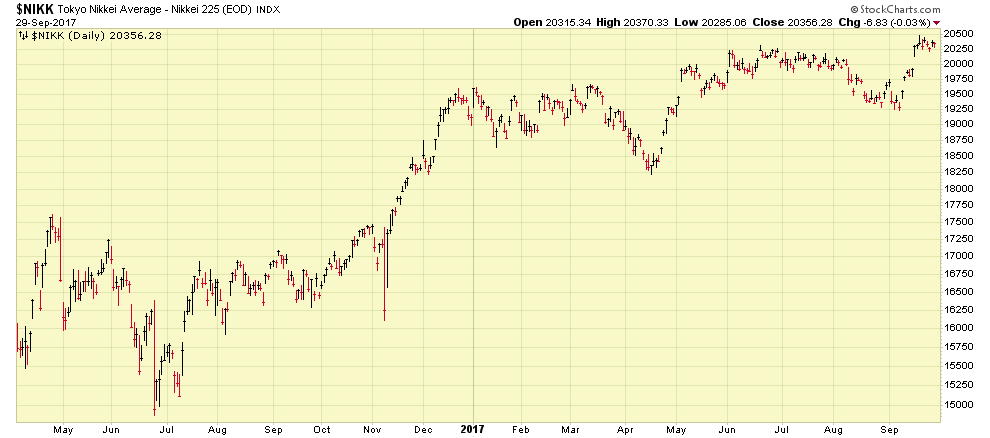

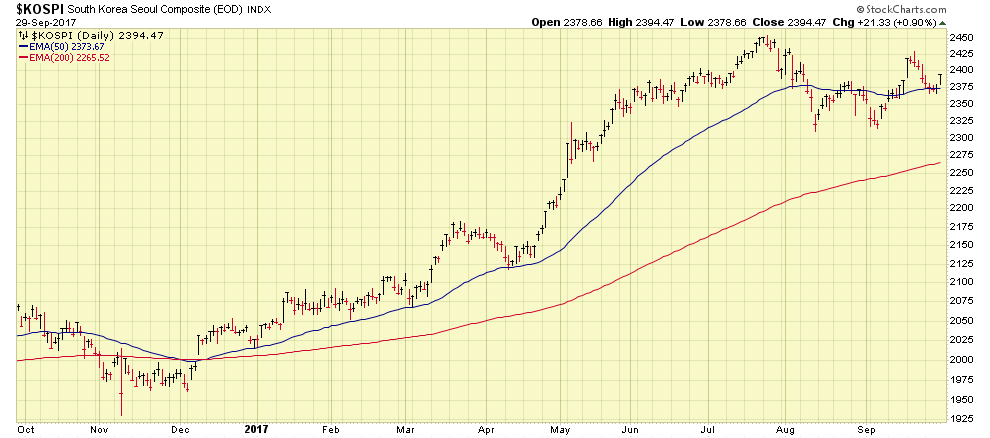

Moving forward, and returning to the topic of this post, the markets performed very well in October. My default, market health barometer, the SP 500 Index, made new highs, as did international stocks to include North Korea neighbors of South Korea KOSPI Index and the Japan Nikkei Index. While the threats from North Korea are clearly a worrisome matter, the Asian markets have apparently discounted them and returned to regular programming- the aforementioned Asia indexes are uptrending nicely. See charts with comments:

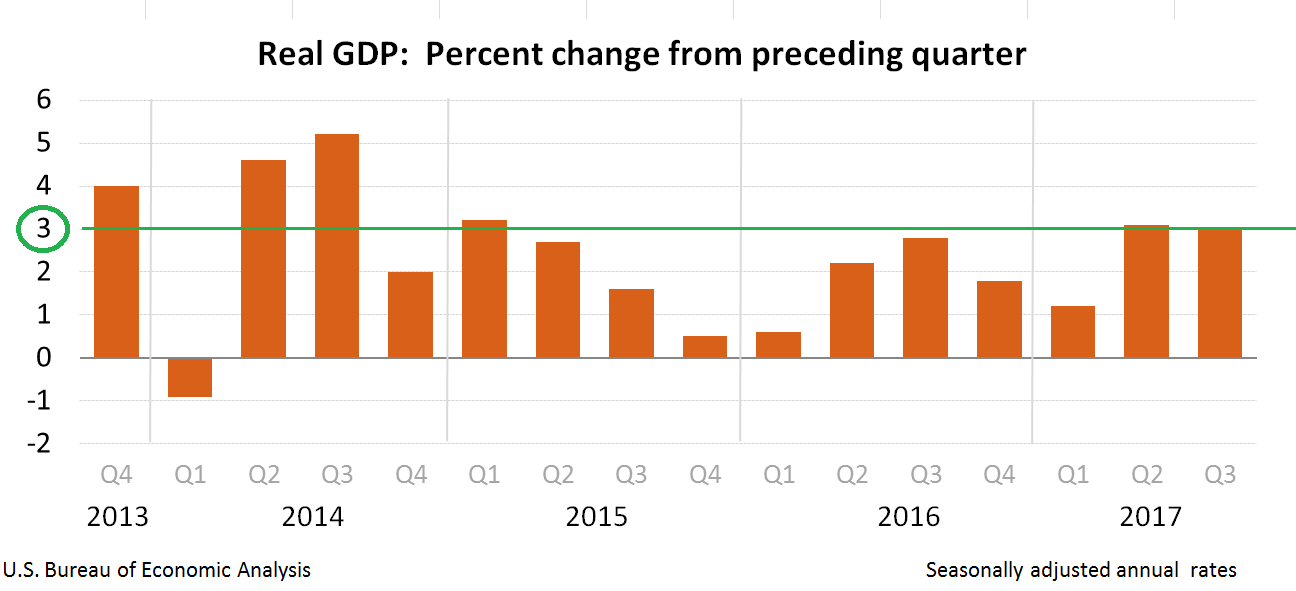

Traveling back home, the US markets are doing very well. Primary causal factor is the improving Gross Domestic Product (GDP). GDP is important because it gives information about the size of the economy and how an economy is performing. The growth rate of real GDP is often used as an indicator of the general health of the economy. In broad terms, an increase in real GDP is interpreted as a sign that the economy is doing well. Note that in July, FOMC Chairwoman Janet Yellen advised Congress that achieving 3% GDP would be difficult. However recent GDP statistics from the Bureau of Economic Analysis indeed appear very positive, third quarter GDP of 3%, previous quarter of 3.1%. See chart:

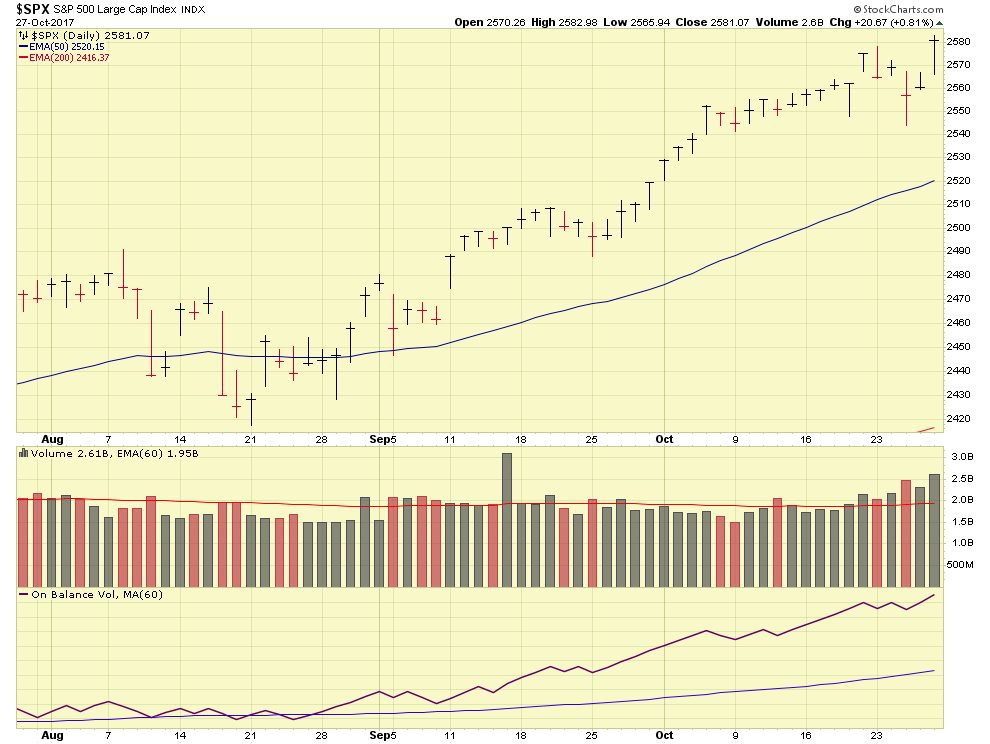

Remember, many believe (including me) that the markets are a leading indicator, in other words, they go up (and down), long before the general public understands why. We saw this in the 2000 market crash, and the 2009 bull market, the market direction changed before most of the audience identified what was happening. What does that mean for us ? It means that the current uptrend may be indicative of a longer term bull cycle. Indeed many have observed that “this never happened before” and believe that the current market is “ready for a pullback” but when in doubt, follow the market itself. Let’s take a look at some SP 500 Charts:

As mentioned earlier, my TSP Allocation remains the same. Varying my analysis from different look-back periods, 90 days, 30-days, to weekly, I find it difficult to make “performance tweaks” to my TSP- all the funds are doing quite well. Looking ahead, the following dates/events may be noteworthy in the coming weeks:

New pick for FOMC Chairperson: Expected Oct-30 week

Ways and Means Chairman Kevin Brady introduces Tax Reform Bill: Nov-1

POTUS Asia Tour: Nov 3-14

Congress Thanksgiving Break: Nov-18 to Nov-26

Note that it is my opinion that if the Tax Reform proposals pass, the stock markets will respond with enthusiasm. Further note that historically, November thru April represents a historically positive phase/cycle, the markets are typically up every month during that time period.

Nothing further to report for now….please continue to share my website with your friends and colleagues, I find it quite rewarding that I am able to raise awareness and share my point of view in regards to the markets and the TSP in general. Once again, go take a look at Dan Jamison’s site and make sure you subscribe to his newsletter.

Thanks for reading…..

-Bill Pritchard